Adding a Co-Signer to Your Car Lease

Understanding the Need for a Co-Signer on Your Car Lease Agreement

So, you're thinking about adding a co-signer to your car lease, huh? Maybe you're having trouble getting approved on your own, or perhaps you just want a little extra security. Whatever the reason, adding a co-signer can be a smart move. But before you jump in, let's break down why you might need one in the first place. Often, it boils down to credit history. Lenders, the folks holding the keys to your dream car (well, leasing it to you, anyway), want to see that you're a responsible borrower. That means a solid credit score and a history of paying your bills on time. If your credit is less than stellar, or if you're just starting out and haven't built much credit yet, a co-signer can significantly improve your chances of getting approved. They're essentially vouching for you, saying, "Hey, I trust this person to make their payments, and if they don't, I'll cover it." It’s a big responsibility for them, so make sure you’re upfront about your financial situation.

Finding the Right Co-Signer for Your Car Lease Application

Alright, you've decided a co-signer is the way to go. Now comes the tricky part: finding the right person. This isn't just about asking your best friend or your favorite aunt. A good co-signer needs to have a few key qualities, the most important being good credit. Think of it like this: their credit score is like a golden ticket. The higher the score, the better your chances of getting approved for the lease, and potentially at a lower interest rate. They also need to have a stable income. Lenders want to see that they can realistically afford to make your car payments if you can't. And finally, and maybe most importantly, they need to be someone you trust and someone who trusts you. This is a serious financial commitment, and it can strain relationships if things go south. Have an open and honest conversation with potential co-signers about your situation, your ability to make payments, and what happens if you can't. Clear communication is key to avoiding headaches down the road.

The Co-Signer's Responsibilities and Legal Implications in a Car Lease

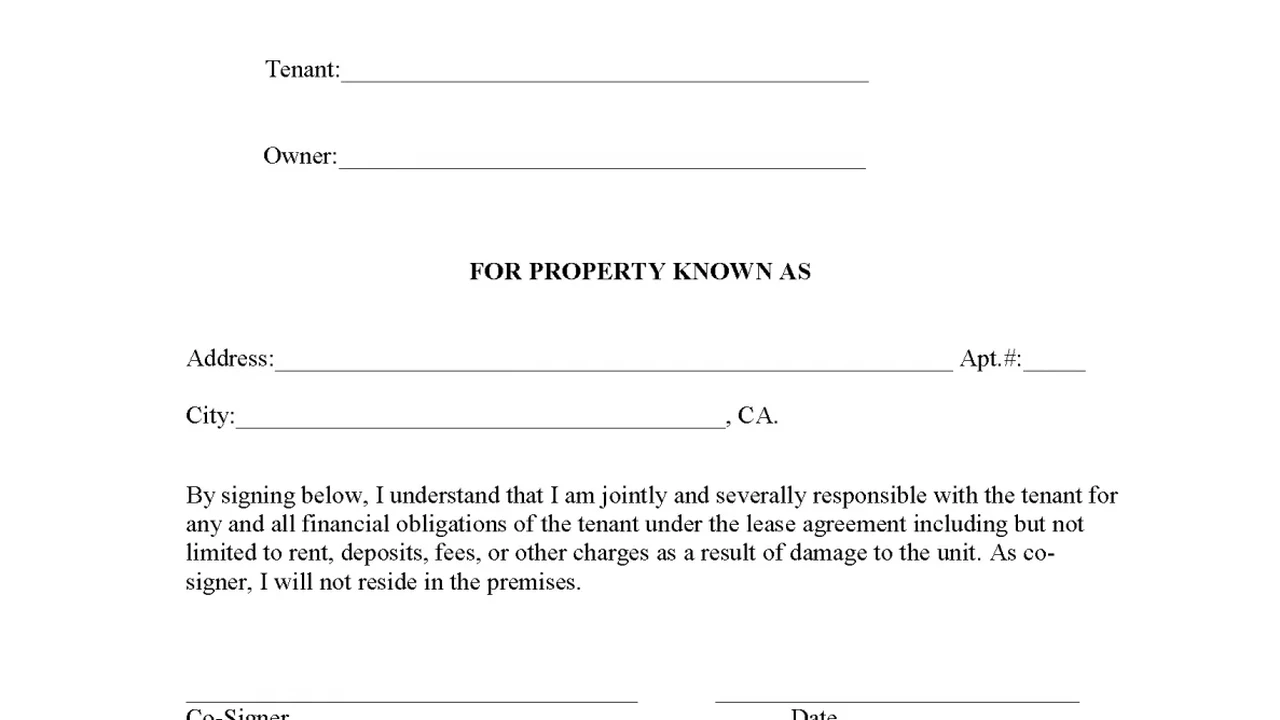

Okay, let's get down to the nitty-gritty: what exactly does a co-signer sign up for? In short, they're legally responsible for the car lease just as much as you are. That means if you miss a payment, they're on the hook for it. If you completely default on the lease, they're responsible for the remaining balance and any associated fees. And it doesn't stop there. The missed payments or default will also negatively impact their credit score, making it harder for them to get loans or credit cards in the future. It’s crucial that your co-signer understands these responsibilities before they sign anything. They should carefully review the lease agreement and ask questions about anything they don't understand. They should also keep a copy of the agreement for their records. Think of it this way: they're not just helping you get a car; they're putting their financial reputation on the line.

Step-by-Step Guide to Adding a Co-Signer to Your Car Lease Agreement

Ready to take the plunge? Here's a step-by-step guide to adding a co-signer to your car lease:

- Find a Co-Signer: As we discussed, choose someone with good credit and a stable income.

- Discuss the Details: Have an open and honest conversation about the responsibilities and potential risks.

- Complete the Application: Both you and your co-signer will need to fill out the lease application, providing personal and financial information.

- Credit Check: The lender will run credit checks on both of you.

- Review the Agreement: Carefully review the lease agreement together, paying attention to the terms, interest rate, and payment schedule.

- Sign the Agreement: Once you're both comfortable, sign the lease agreement.

- Keep a Copy: Make sure you both have a copy of the signed agreement for your records.

Navigating Co-Signer Requirements and Car Lease Approval Process

Each lender has its own specific requirements for co-signers, so it's important to do your research. Some lenders may require a higher credit score than others, or they may have specific income requirements. Before you even start the application process, call the lender and ask about their co-signer requirements. This can save you a lot of time and frustration. Also, be prepared to provide documentation to support your application. This might include pay stubs, bank statements, and proof of address. The more information you can provide, the smoother the approval process will be. And remember, honesty is always the best policy. Don't try to hide anything from the lender, as this could jeopardize your application.

Co-Signer Release Options and Removing a Co-Signer From a Car Lease

Okay, so what happens down the road? Is your co-signer stuck with you for the entire lease term? Not necessarily. Some leases allow you to release your co-signer after a certain period of time, provided you meet certain criteria. This usually involves making a certain number of on-time payments and demonstrating that you're financially stable enough to handle the lease on your own. Check your lease agreement to see if it includes a co-signer release option. If it does, find out what the requirements are and what steps you need to take to initiate the release process. If your lease doesn't include a release option, you might be able to refinance the lease in your name only, effectively removing the co-signer. This will require you to qualify for a new lease based on your own credit and income. It’s worth exploring both options to give your co-signer some peace of mind.

Potential Risks and Downsides of Having a Co-Signer on Your Car Lease

While a co-signer can be a lifesaver, it's not without its risks. For you, the biggest risk is damaging your relationship with your co-signer if you fail to make your payments. Remember, they're putting their trust in you, and you don't want to let them down. For the co-signer, the risks are even greater. They're potentially liable for your debt, and their credit score could take a hit if you miss payments. They also might find it harder to get loans or credit cards themselves while they're co-signing for you. It’s really important to weigh these risks carefully before deciding to add a co-signer. Consider all your options and make sure you're both fully aware of the potential consequences.

Alternatives to Using a Co-Signer for Car Lease Approval

Before you commit to a co-signer, explore some alternatives. One option is to save up a larger down payment. This can reduce the amount you need to borrow, making it easier to get approved. Another option is to look for a less expensive car. You might not get your dream car right away, but it's better to have a reliable car you can afford than to struggle with payments on a more expensive one. You could also try to improve your credit score before applying for the lease. This might involve paying down existing debt, disputing errors on your credit report, or becoming an authorized user on someone else's credit card. Finally, consider shopping around for different lenders. Some lenders are more willing to work with people with less-than-perfect credit than others. Don't just settle for the first offer you get. Take the time to compare rates and terms from multiple lenders.

Building Credit While Leasing a Car With a Co-Signer

Leasing a car with a co-signer can actually be a great way to build your credit. Every time you make an on-time payment, it gets reported to the credit bureaus, which can help improve your credit score. Make sure you're making your payments on time every month. You can even set up automatic payments to avoid missing a due date. Also, keep your credit utilization low. This means keeping the balances on your credit cards low relative to your credit limits. By managing your credit responsibly while leasing a car, you can build a solid credit history and qualify for better rates on loans and credit cards in the future. Think of it as an investment in your financial future.

Negotiating Lease Terms and Interest Rates With a Co-Signer

Having a co-signer can give you more leverage when negotiating lease terms and interest rates. Since the lender sees you as a lower risk, they might be willing to offer you a better deal. Don't be afraid to negotiate. Ask for a lower interest rate, a shorter lease term, or a lower monthly payment. You can also negotiate the price of the car. Remember, everything is negotiable. Do your research and know what the fair market value of the car is. Come prepared with data to support your arguments. And don't be afraid to walk away if you're not happy with the offer. There are plenty of other dealerships out there.

Maintaining a Positive Relationship With Your Car Lease Co-Signer

This is probably the most important part. Adding a co-signer is a huge ask, and it’s vital to maintain a positive relationship with them throughout the lease term. Communicate openly and honestly about your financial situation. Keep them informed of any changes that might affect your ability to make payments. Thank them for their help and support. And most importantly, make your payments on time. By being a responsible borrower and a good friend, you can ensure that your co-signer relationship remains strong and positive.

Real-Life Examples of Successful Co-Signer Car Lease Scenarios

Let’s look at a few examples. Sarah, a recent college graduate, needed a car to get to her new job. She had limited credit history, so her mom co-signed her lease. Sarah made all her payments on time, and after two years, she was able to refinance the lease in her own name, releasing her mom from the obligation. Then there's Mark, who had some past credit problems. His brother co-signed his lease, giving him a second chance. Mark used the opportunity to rebuild his credit, and he's now well on his way to financial stability. These are just a few examples of how a co-signer can help you get a car and improve your financial situation. Remember, it's all about responsible borrowing and open communication.

Legal Protections for Co-Signers and Car Lease Agreements

Co-signers actually have some legal protections. In many states, lenders are required to notify co-signers if the primary borrower misses a payment. This gives the co-signer an opportunity to step in and make the payment to avoid further damage to their credit. Co-signers also have the right to receive copies of all loan documents and to be informed of any changes to the loan terms. It's important for co-signers to know their rights and to exercise them if necessary. If you're considering becoming a co-signer, research the laws in your state to understand your protections.

Frequently Asked Questions About Car Leases and Co-Signers

Let's tackle some common questions:

- Q: Can I add a co-signer after I've already signed the lease? A: Usually not. You typically need the co-signer at the time of application.

- Q: Does a co-signer have any ownership rights to the car? A: No, the co-signer is only responsible for the debt, not the ownership of the vehicle.

- Q: What happens if the primary borrower files for bankruptcy? A: The co-signer is still responsible for the debt, even if the primary borrower files for bankruptcy.

- Q: Can I use more than one co-signer? A: Some lenders may allow this, but it's not common.

Product Recommendations for Maintaining Your Leased Car

Alright, let's talk about keeping your leased car in tip-top shape! Remember, you'll be returning it eventually, and you want to avoid those nasty end-of-lease fees. Here are a few products I recommend:

Car Wash Soap: Meguiar's Gold Class Car Wash Shampoo & Conditioner

Use Case: Regular washing is key to preventing paint damage. This soap is gentle yet effective at removing dirt and grime. Comparison: Cheaper soaps can strip away wax and damage your paint. Meguiar's is pH balanced and safe for all finishes. Price: Around $10-$15 per bottle.

Interior Cleaner: Armor All Protectant Wipes

Use Case: Keeps your dashboard, console, and door panels clean and protected from UV damage. Comparison: Sprays can be messy and leave streaks. Wipes are convenient and easy to use. Price: Around $8-$12 per container.

Floor Mats: WeatherTech FloorLiners

Use Case: Protects your car's carpets from dirt, mud, and spills. Essential for avoiding wear and tear. Comparison: Universal floor mats often don't fit properly and can shift around. WeatherTech FloorLiners are custom-molded for your specific car model. Price: Around $100-$200 per set, depending on the vehicle.

Tire Pressure Gauge: Accutire MS-4021B Digital Tire Pressure Gauge

Use Case: Maintaining proper tire pressure improves fuel efficiency and extends tire life. Crucial for a smooth and safe ride. Comparison: Analog gauges can be difficult to read accurately. Digital gauges provide precise readings. Price: Around $10-$15.

Leather Conditioner (if applicable): Lexol Leather Conditioner

Use Case: Prevents leather seats from drying out and cracking. Keeps them looking and feeling new. Comparison: Some leather conditioners can leave a greasy residue. Lexol absorbs quickly and leaves a natural finish. Price: Around $15-$20 per bottle.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)