Buying a Car Outright vs. Car Leasing

Understanding Your Car Ownership Options Direct Purchase vs Car Leasing

Okay, so you're in the market for a new ride, right? Awesome! But before you get swept away by that shiny new car smell, let's talk about the nitty-gritty: how you're actually going to *get* that car. The two big contenders are buying it outright and leasing it. They're totally different beasts, and what works for your neighbor Steve might be a complete disaster for you. We're going to break down the pros and cons of each so you can make the smartest choice for your wallet and your lifestyle.

Buying outright means, well, exactly that. You own the car. You either pay cash (if you're rolling in dough, good for you!) or, more likely, you take out an auto loan. You make payments for a set period, and once you've paid it off, the car is all yours, free and clear. Leasing, on the other hand, is more like a long-term rental. You pay a monthly fee to use the car for a specific period (usually 2-3 years), and at the end of the lease, you return it. Think of it like renting an apartment versus buying a house.

Financial Breakdown Direct Car Purchase vs Car Leasing Cost Comparison

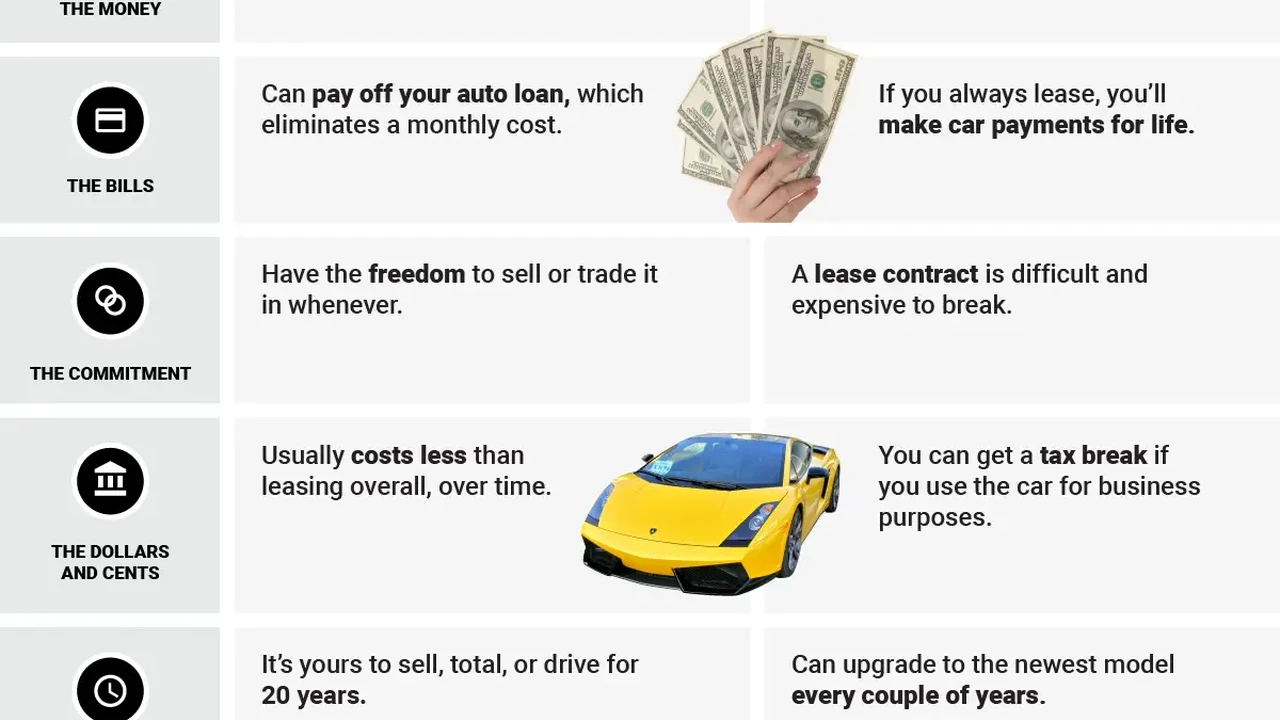

Let's get down to brass tacks: the money. Buying a car usually involves a larger upfront cost. You'll need a down payment, plus taxes and fees. Then there are the monthly loan payments, which include principal and interest. On the plus side, once you've paid off the loan, you own the car. You can drive it until the wheels fall off (literally!), and you can sell it later to recoup some of your investment.

Leasing often has a lower upfront cost. Sometimes you can even lease with no money down! The monthly payments are typically lower than loan payments because you're only paying for the depreciation of the car during the lease term. However, at the end of the lease, you have nothing to show for it. You have to return the car, and you're back to square one. Also, leasing agreements often come with mileage restrictions. Go over your allotted miles, and you'll be slapped with hefty fees.

Long Term Ownership Car Purchase Benefits vs Car Leasing Drawbacks

Think long-term. When you buy a car, you build equity. It's an asset you can sell later. You also have the freedom to customize it, drive it as much as you want, and keep it for as long as you want. The downside? Cars depreciate, meaning they lose value over time. You're also responsible for all maintenance and repairs, which can get expensive.

Leasing is great if you like driving a new car every few years. You get to enjoy the latest technology and safety features without the hassle of selling your old car. Plus, most leases include maintenance coverage, so you don't have to worry about routine service. The downside? You never actually own the car. You're always making payments, and you're limited by mileage restrictions and lease terms. And if you want to end the lease early, you'll likely face significant penalties.

Mileage Considerations High Mileage vs Low Mileage Drivers Car Buying and Leasing

Are you a road warrior or a weekend driver? If you rack up a lot of miles, buying is probably the better option. Lease agreements typically have mileage limits (e.g., 10,000, 12,000, or 15,000 miles per year). Go over that limit, and you'll pay a per-mile charge, which can quickly add up. If you only drive a few miles a year, leasing might be a good fit, but make sure the mileage allowance is sufficient.

Customization Options Modifying Your Car When Buying vs Leasing

Do you dream of adding a spoiler, upgrading the sound system, or tinting the windows? If so, buying is the way to go. When you own the car, you can customize it to your heart's content. Leasing agreements typically prohibit modifications. You have to return the car in its original condition, or you'll be charged for any alterations.

Maintenance and Repairs Who Pays When Buying vs Leasing a Car

When you buy a car, you're responsible for all maintenance and repairs, from oil changes to major engine work. This can be a significant expense, especially as the car gets older. Leasing often includes maintenance coverage for routine service, such as oil changes and tire rotations. However, you're still responsible for things like tires, brakes, and damage from accidents.

Resale Value and Depreciation Maximizing Value When Buying or Leasing

Cars depreciate. It's a fact of life. When you buy a car, you bear the brunt of that depreciation. You might be able to recoup some of your investment when you sell the car, but it will likely be for less than you paid for it. With leasing, you don't have to worry about depreciation. You're only paying for the portion of the car's value that you use during the lease term. However, you also don't get any money back at the end of the lease.

Credit Score Impact Car Loan vs Lease Approval Requirements

Your credit score plays a big role in both buying and leasing a car. A good credit score will qualify you for lower interest rates on a car loan and better lease terms. If you have a poor credit score, you might have trouble getting approved for either a loan or a lease, or you might have to pay higher interest rates or fees.

Specific Car Recommendations for Different Needs and Budgets

Okay, let's get into some actual cars! Here are a few recommendations based on different needs and budgets:

For the Budget-Conscious Buyer: The Kia Rio

If you're looking for a reliable and affordable car, the Kia Rio is a great option. It's fuel-efficient, comes with a generous warranty, and has a surprisingly spacious interior for a subcompact car. You can often find a new Rio for under $20,000. It's perfect for commuting, running errands, and basic transportation.

For the Practical Family: The Toyota RAV4

The Toyota RAV4 is a perennial favorite for families, and for good reason. It's spacious, safe, reliable, and fuel-efficient. It also has plenty of cargo space for groceries, sports equipment, or luggage. Prices start around $28,000, but you'll get a lot of value for your money. Great for road trips, school runs, and everything in between.

For the Eco-Friendly Driver: The Tesla Model 3

If you're looking to reduce your carbon footprint and enjoy a cutting-edge driving experience, the Tesla Model 3 is a top contender. It's an all-electric sedan with impressive range, performance, and technology. Prices start around $45,000, but you'll save money on gas and maintenance in the long run. Ideal for environmentally conscious drivers who want a stylish and fun-to-drive car.

For the Adventurer: The Subaru Outback

If you love exploring the great outdoors, the Subaru Outback is a rugged and capable wagon that's perfect for adventure. It has standard all-wheel drive, plenty of ground clearance, and a spacious interior. Prices start around $27,000. Perfect for camping, hiking, skiing, and exploring off the beaten path.

Comparing the Options Key Factors to Consider for Car Buying and Leasing

Let's break down the key differences in a table:

| Feature | Buying | Leasing |

|---|---|---|

| Ownership | You own the car | You rent the car |

| Upfront Cost | Higher (down payment, taxes, fees) | Lower (sometimes no money down) |

| Monthly Payments | Usually higher | Usually lower |

| Mileage Restrictions | None | Limited |

| Customization | Allowed | Usually prohibited |

| Maintenance | Your responsibility | Often included |

| Resale Value | Potential to recoup some investment | None |

Real World Examples of Car Buying and Leasing Scenarios

Okay, let's look at some real-world examples. Sarah needs a car for her daily commute to work, which is about 50 miles each way. She drives a lot! Buying would likely be a better option for her, as she wouldn't have to worry about mileage restrictions. She could buy a used Toyota Camry for around $15,000 and drive it for several years.

John, on the other hand, only drives a few miles a week. He likes having a new car every few years and doesn't want to deal with the hassle of maintenance. Leasing would probably be a better fit for him. He could lease a Honda Civic for around $250 a month and enjoy a new car every three years.

Depreciation Explained How Car Value Changes Over Time

Understanding depreciation is key. A new car loses a significant portion of its value in the first few years. This is why some people prefer to buy slightly used cars, letting someone else take the initial depreciation hit. Leasing avoids this concern, as you're only paying for the car's depreciation during the lease term. However, you never own the asset, so you don't benefit from any residual value.

Negotiating Tips for Car Loans and Leases Getting the Best Deal

Whether you're buying or leasing, negotiation is key. Do your research, know the market value of the car you're interested in, and be prepared to walk away if the dealer isn't willing to give you a fair price. For loans, shop around for the best interest rates. For leases, pay close attention to the money factor (which is similar to an interest rate) and the residual value (the estimated value of the car at the end of the lease). Don't be afraid to negotiate these terms!

Hidden Costs and Fees To Watch Out For When Buying or Leasing

Beware of hidden costs and fees! When buying, watch out for things like dealer prep fees, documentation fees, and extended warranties. When leasing, be aware of disposition fees (a fee charged when you return the car), excess wear and tear charges, and early termination fees. Read the fine print carefully and ask questions about anything you don't understand.

Making the Right Choice Your Personal Car Buying and Leasing Guide

Ultimately, the decision of whether to buy or lease is a personal one. There's no right or wrong answer. Consider your individual needs, budget, and lifestyle. Do your research, compare your options, and make the choice that's best for you. Good luck finding your perfect ride!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)