Car Leasing and Insurance: What You Need to Know

Understanding Car Leasing Insurance Requirements Key Considerations

So, you're thinking about leasing a car? Awesome! It's a great way to drive a new vehicle without the long-term commitment of buying. But before you sign on the dotted line, let's talk about something crucial: insurance. Leasing companies require you to have specific insurance coverage to protect their asset (the car!). Don't worry, it's not as scary as it sounds. We'll break it down.

Generally, you'll need full coverage, which includes:

- Liability Insurance: This covers damages you cause to other people or their property in an accident. States have minimum liability requirements, but leasing companies often require higher limits. Think of it as protecting yourself from a major financial hit if you're at fault.

- Collision Insurance: This covers damage to your leased vehicle, regardless of who's at fault. Even if another driver crashes into you, collision insurance will help pay for the repairs. Your leasing company will definitely want this!

- Comprehensive Insurance: This covers damage to your leased vehicle from things other than collisions, like theft, vandalism, fire, hail, or even hitting a deer. It's a good safety net for unexpected events.

It's important to note that these are general guidelines. Your specific leasing agreement will outline the exact insurance requirements. Read it carefully! And don't hesitate to ask the leasing company for clarification if anything is unclear. They're there to help.

Shopping for Car Leasing Insurance Finding the Best Rates and Coverage

Okay, so you know what kind of insurance you need. Now comes the fun part: shopping around! Don't just settle for the first quote you get. Insurance rates can vary significantly between companies, so it pays to do your homework.

Here are some tips for finding the best rates and coverage:

- Get Multiple Quotes: Contact several different insurance companies (both online and local) and request quotes for the required coverage. Websites like Progressive, Geico, and State Farm are good starting points.

- Compare Apples to Apples: Make sure you're comparing the same coverage levels and deductibles when comparing quotes. A lower premium might seem appealing, but it could come with a higher deductible, meaning you'll pay more out-of-pocket if you have an accident.

- Ask About Discounts: Many insurance companies offer discounts for things like having multiple policies (e.g., home and auto), being a safe driver, or having anti-theft devices installed in your car. Don't be afraid to ask what discounts you're eligible for.

- Consider a Higher Deductible: Choosing a higher deductible can lower your premium. Just make sure you can comfortably afford to pay that deductible if you have an accident.

- Check Your Credit Score: In many states, insurance companies use your credit score to determine your premium. A good credit score can help you get a better rate.

Remember, the cheapest insurance isn't always the best. You want to make sure you have adequate coverage to protect yourself and your leased vehicle. Think about the potential financial consequences of an accident and choose a policy that provides sufficient protection.

Gap Insurance for Car Leases Protecting Yourself from Financial Loss

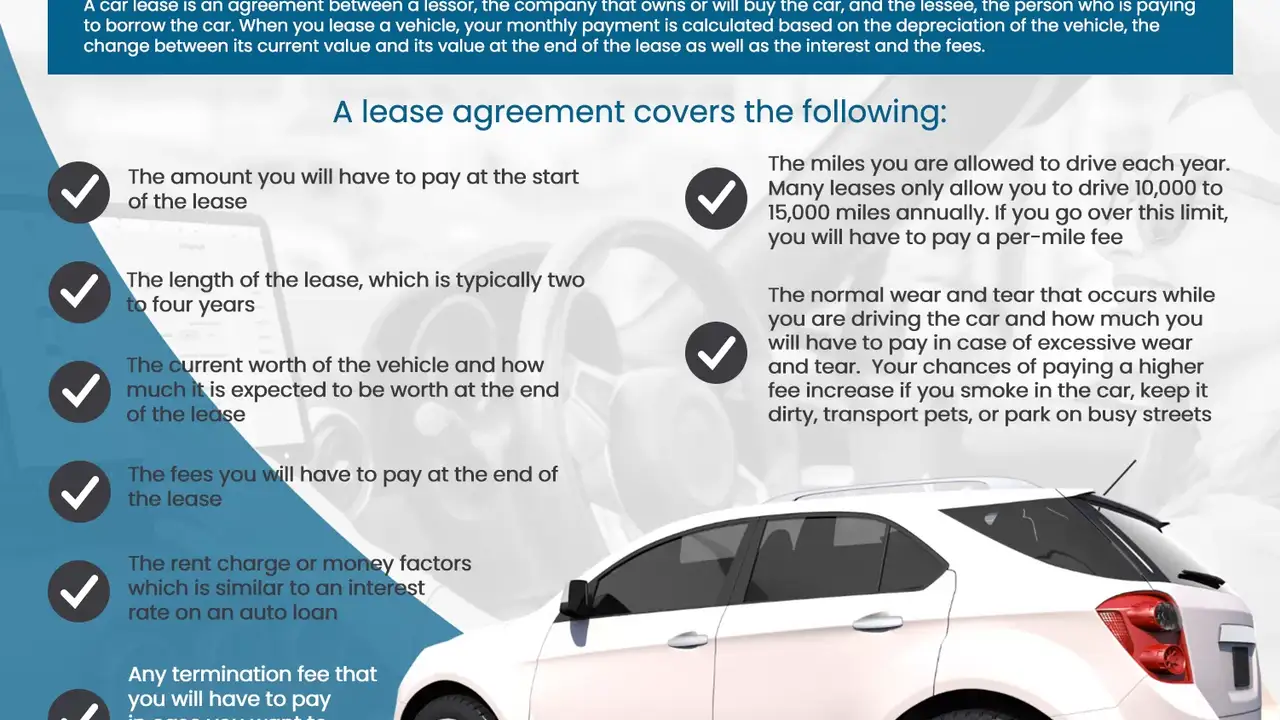

Here's where things get a little more complicated, but it's super important to understand: Gap insurance. Gap insurance stands for "Guaranteed Asset Protection," and it covers the "gap" between what you owe on your lease and what the car is actually worth if it's totaled or stolen.

Why is this important? Cars depreciate quickly, especially in the first few years. If you total your leased car a year into the lease, the insurance company will only pay the car's current market value. But you're still responsible for paying off the remaining lease balance, which could be significantly higher than the car's value. That's where gap insurance comes in.

Gap insurance typically covers the difference between:

- The outstanding balance on your lease

- The car's actual cash value (ACV) at the time of the loss

Many leasing companies require you to purchase gap insurance. Even if they don't, it's highly recommended. It's a relatively inexpensive way to protect yourself from a potentially large financial loss. You can usually purchase gap insurance from the leasing company or from your auto insurance provider. Compare pricing from both to get the best deal.

Specific Car Leasing Scenarios and Insurance Considerations Real-World Examples

Let's look at some real-world scenarios to illustrate how insurance works with car leases:

Scenario 1: Minor Fender Bender

You're backing out of a parking space and accidentally bump into another car, causing minor damage to both vehicles. Your liability insurance will cover the damage to the other car. If you're at fault, you'll likely have to pay your deductible for your collision insurance to cover the damage to your leased car. Your insurance company will handle the claims process and negotiate with the other driver's insurance company.

Scenario 2: Totaled Car Due to an Accident

You're involved in a serious accident, and your leased car is totaled. Your collision insurance will cover the actual cash value (ACV) of the car. If you have gap insurance, it will cover the difference between the ACV and the remaining lease balance. Without gap insurance, you would be responsible for paying that difference out of pocket.

Scenario 3: Car Stolen

Your leased car is stolen. Your comprehensive insurance will cover the actual cash value (ACV) of the car. Again, gap insurance will cover the difference between the ACV and the remaining lease balance.

Scenario 4: Damage from a Hailstorm

A severe hailstorm damages your leased car. Your comprehensive insurance will cover the cost of repairing the damage. You'll likely have to pay your deductible.

These scenarios highlight the importance of having adequate insurance coverage when leasing a car. It's not just about meeting the leasing company's requirements; it's about protecting yourself from financial risk.

Recommended Car Models and Insurance Cost Considerations for Leasing

When choosing a car to lease, consider how the make and model will impact your insurance costs. Certain vehicles tend to have higher insurance premiums due to factors like their popularity with thieves, the cost of repairs, and their safety ratings.

Lower Insurance Cost Options:

- Toyota Corolla: Known for its reliability and safety, the Corolla typically has lower insurance rates. A 2023 Corolla LE can be leased for around $250-$350 per month, and insurance might range from $100-$150 per month, depending on your driving record and location. Great for daily commuting and fuel efficiency.

- Honda Civic: Similar to the Corolla, the Civic is a safe and dependable choice with relatively affordable insurance. A 2023 Civic LX lease might cost $275-$375 per month, with insurance in a similar range as the Corolla. A versatile option for city driving and weekend trips.

- Subaru Impreza: With standard all-wheel drive and a reputation for safety, the Impreza often enjoys favorable insurance rates. A 2023 Impreza base model lease could be around $290-$390 per month, with insurance costs potentially slightly higher than the Corolla and Civic due to the AWD system. Ideal for areas with snowy or icy conditions.

Higher Insurance Cost Options (Consider Carefully):

- Nissan Altima: While a popular sedan, the Altima sometimes has higher insurance rates due to its theft rates and repair costs. A 2023 Altima S lease might be in the $300-$400 range, but insurance could easily exceed $175-$250 per month, especially for younger drivers.

- Dodge Charger: This muscle car is known for its performance, but also for its higher insurance premiums. A 2023 Charger SXT lease could be around $400-$550 per month, and insurance could be significantly higher than other sedans, often exceeding $250 per month. Only recommended if you're willing to pay the higher insurance costs.

- Luxury SUVs (e.g., BMW X5, Mercedes-Benz GLE): While offering premium features and performance, luxury SUVs come with higher insurance costs due to their high repair costs and target theft rates. Lease prices vary greatly depending on the model and trim, but insurance can easily be $300+ per month.

Factors Affecting Insurance Cost: Your age, driving record, location, and the specific coverages you choose will all impact your insurance premium. Always get a quote for the specific car you're considering before signing a lease.

Comparing Car Leasing Insurance Providers Choosing the Right Company for Your Needs

There are tons of insurance companies out there, each with its own strengths and weaknesses. Here's a quick comparison of some popular providers:

- Progressive: Known for its online tools and competitive rates, Progressive is a good option for comparing quotes from multiple companies. They often offer discounts for bundling policies.

- Geico: Geico is another large insurer with a reputation for affordable rates. They offer a variety of discounts and have a user-friendly website and mobile app.

- State Farm: State Farm is a well-established insurer with a strong network of local agents. They offer personalized service and a wide range of insurance products.

- Allstate: Allstate is another major insurer with a comprehensive range of coverage options. They offer discounts for safe driving and loyalty.

- Local and Regional Insurers: Don't overlook smaller, local insurance companies. They may offer more personalized service and competitive rates for your specific area.

When comparing insurance providers, consider factors like:

- Price: Get quotes from multiple companies and compare the premiums.

- Coverage Options: Make sure the company offers the coverage you need, including liability, collision, comprehensive, and gap insurance.

- Discounts: Ask about available discounts and see if you qualify.

- Customer Service: Read online reviews and check the company's customer service ratings.

- Claims Process: Find out how the company handles claims and what their process is for resolving disputes.

- Financial Stability: Choose an insurer with a strong financial rating to ensure they can pay out claims.

Take your time, do your research, and choose an insurance provider that meets your needs and budget. Leasing a car is a fantastic option, and making sure you are properly covered is the first step to worry-free driving.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)